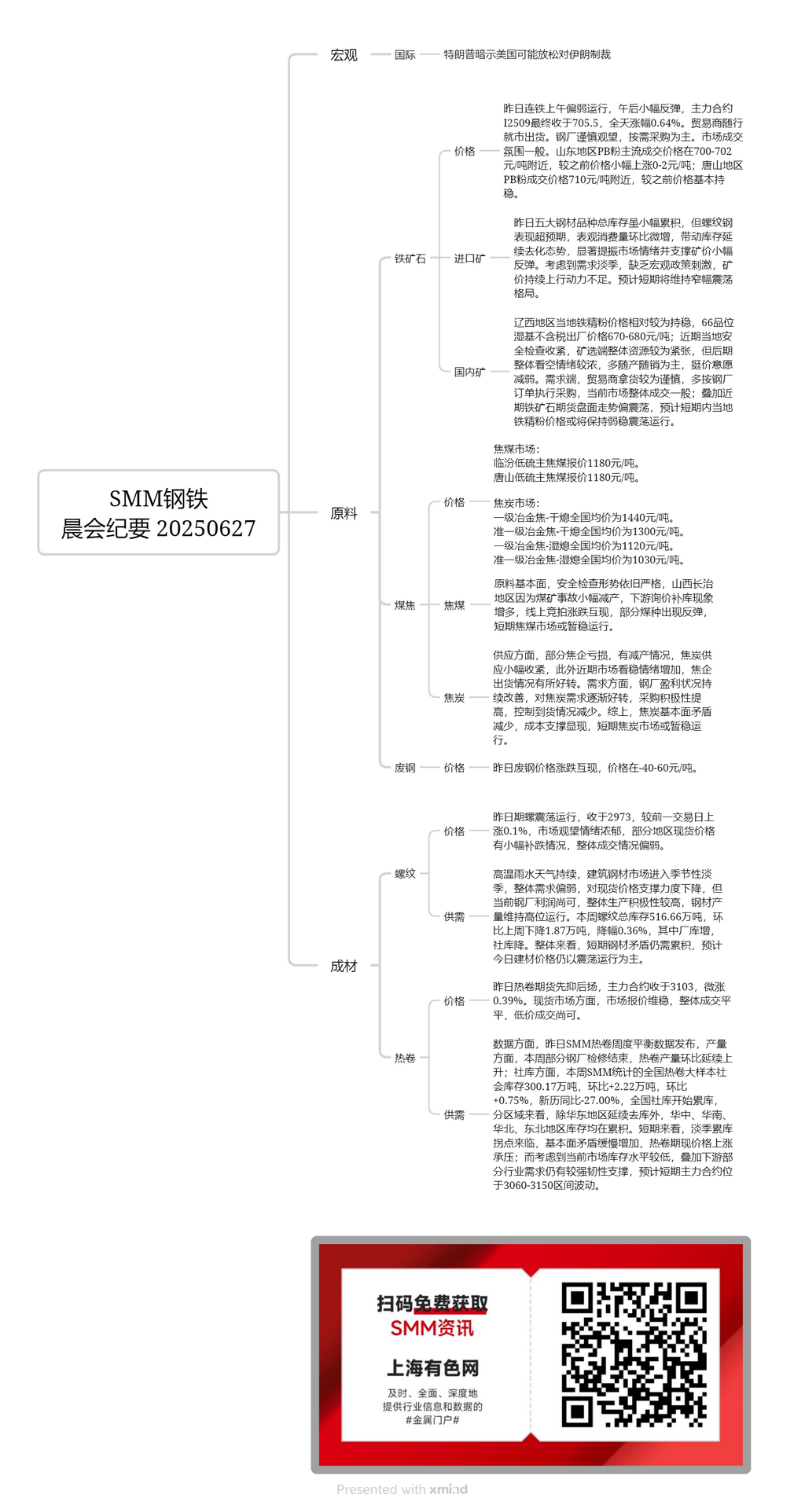

Domestic ore:

In west Liaoning, the local iron ore concentrate prices remained relatively stable. The ex-factory price (66% grade, wet basis, excluding tax) was 670-680 yuan/mt. Recently, local safety inspections have tightened, leading to a relatively tight overall resource situation at mines and beneficiation plants. However, there is a strong bearish sentiment in the market for the later period, with most producers selling as they produce and showing a reduced reluctance to budge on prices. On the demand side, traders are cautious in purchasing and mostly follow steel mill orders for procurement. The overall market transactions are currently average. Coupled with the recent volatile trend in the iron ore futures market, it is expected that the local iron ore concentrate prices will remain weak and stable with oscillatory movements in the short term.

Imported ore:

Yesterday, DCE iron ore futures were weak in the morning session but rebounded slightly in the afternoon. The most-traded contract I2509 closed at 705.5, with a daily increase of 0.64%. Traders sold according to market conditions. Steel mills adopted a wait-and-see approach and purchased as needed. The market transaction atmosphere was average. In Shandong, the mainstream transaction prices of PB fines were around 700-702 yuan/mt, showing a slight increase of 0-2 yuan/mt compared to the previous prices. In Tangshan, the transaction prices of PB fines were around 710 yuan/mt, basically stable compared to the previous prices. Although the total inventory of the five major steel products slightly accumulated yesterday, the performance of rebar exceeded expectations, with a slight MoM increase in apparent consumption, driving the inventory to continue its de-stocking trend. This significantly boosted market sentiment and supported a slight rebound in ore prices. Considering the off-season demand and the lack of macro policy stimulus, there is insufficient upward momentum for ore prices to continue rising. It is expected that ore prices will maintain a narrow oscillatory pattern in the short term.

Coking coal:

The quoted price of low-sulphur coking coal in Linfen is 1,180 yuan/mt. The quoted price of low-sulphur coking coal in Tangshan is 1,180 yuan/mt. Regarding the fundamentals of raw materials, the safety inspection situation remains strict. There has been a slight production cut in the Changzhi area of Shanxi due to a coal mine accident, leading to an increase in downstream inquiries and restocking. Online auctions have shown mixed performance, with some coal types rebounding. The coking coal market may temporarily stabilize in the short term.

Coke:

The nationwide average price of first-grade metallurgical coke (dry quenching) is 1,440 yuan/mt. The nationwide average price of quasi-first-grade metallurgical coke (dry quenching) is 1,300 yuan/mt. The nationwide average price of first-grade metallurgical coke (wet quenching) is 1,120 yuan/mt. The nationwide average price of quasi-first-grade metallurgical coke (wet quenching) is 1,030 yuan/mt. In terms of supply, some coking enterprises are experiencing losses and have cut production, leading to a slight tightening of coke supply. Additionally, the market sentiment has stabilized recently, and the sales situation of coking enterprises has improved. On the demand side, the profitability of steel mills continues to improve, and the demand for coke is gradually picking up, with increased purchasing enthusiasm and reduced control over arrival volumes. In summary, the fundamental contradictions in the coke market have decreased, and cost support has emerged. The coke market may temporarily stabilize in the short term.

Rebar:

Yesterday, rebar futures oscillated and closed at 2,973, up 0.1% from the previous trading day. The market sentiment was characterized by a strong wait-and-see attitude. In some regions, spot prices experienced a slight correction, and overall transaction volumes were weak. The high-temperature and rainy weather persisted, pushing the construction steel market into the off-season. Overall demand remained weak, reducing the support for spot prices. However, steel mill profits were currently moderate, and overall production enthusiasm was high, with steel production continuing to fluctuate at highs. This week, the total rebar inventory stood at 5.1666 million mt, down 18,700 mt WoW, a decrease of 0.36%. Among this, in-plant inventory increased while social inventory decreased. Overall, short-term contradictions in steel still need to accumulate, and it is expected that today's construction material prices will mainly fluctuate.

HRC:

Yesterday, HRC futures first declined and then rose, with the most-traded contract closing at 3103, up slightly by 0.39%. In the spot market, market quotes remained stable, with overall trading being average and low-priced transactions being moderate. In terms of data, SMM released its weekly HRC balance data yesterday. In terms of production, some steel mills completed maintenance this week, and HRC production continued to increase MoM. In terms of social inventory, the large-sample social inventory of HRC nationwide, as compiled by SMM, was 3.0017 million mt this week, up 22,200 mt MoM, an increase of 0.75%, and down 27.00% YoY. Social inventory nationwide began to build up. By region, except for east China, where destocking continued, inventories in central, south, north, and north-east China were all accumulating. In the short term, the turning point for inventory buildup in the off-season has arrived, and contradictions in the fundamentals are slowly increasing, putting pressure on the rise of HRC futures and spot prices. However, considering the currently low market inventory levels and the strong resilience of demand in some downstream industries, it is expected that the most-traded contract will fluctuate within the 3060-3150 range in the short term.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)